-

Top tips for buying a holiday property

15.08.2024 | Bonny GreierAre you thinking about buying a place to spend your holidays? We will explain which financial aspects you should consider, the tax implications of this type of purchase, and the various options available.

Top tips for buying a holiday property

Buying a holiday property – what should you consider?

As a rule, similar calculation methods are used for the financing and tax aspects of a holiday property as for your primary residence. Nevertheless, there are some aspects that differ and these must be borne in mind when buying a holiday property. In addition, buying property in Switzerland is different from buying property abroad.

Buying a holiday property in Switzerland

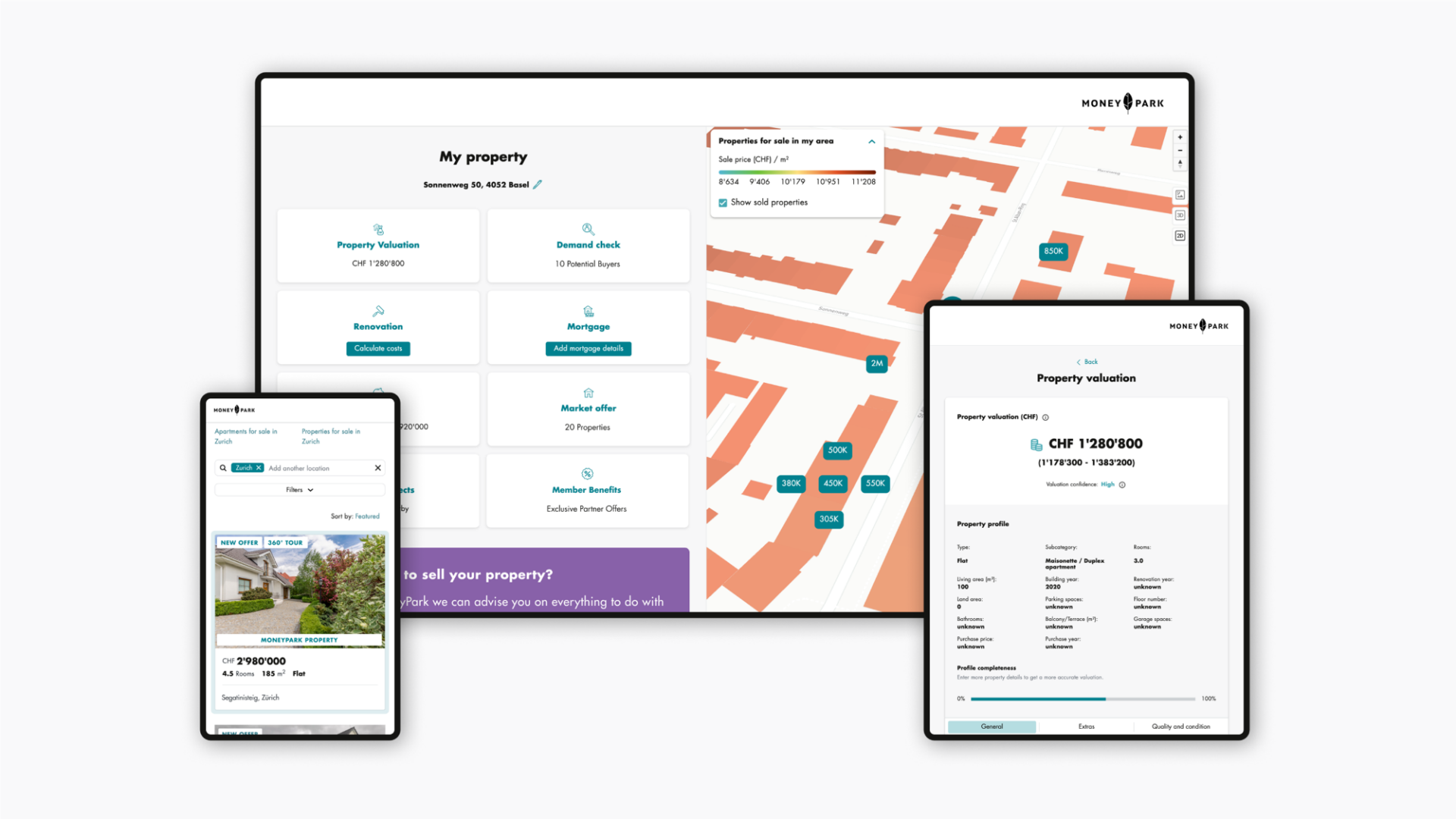

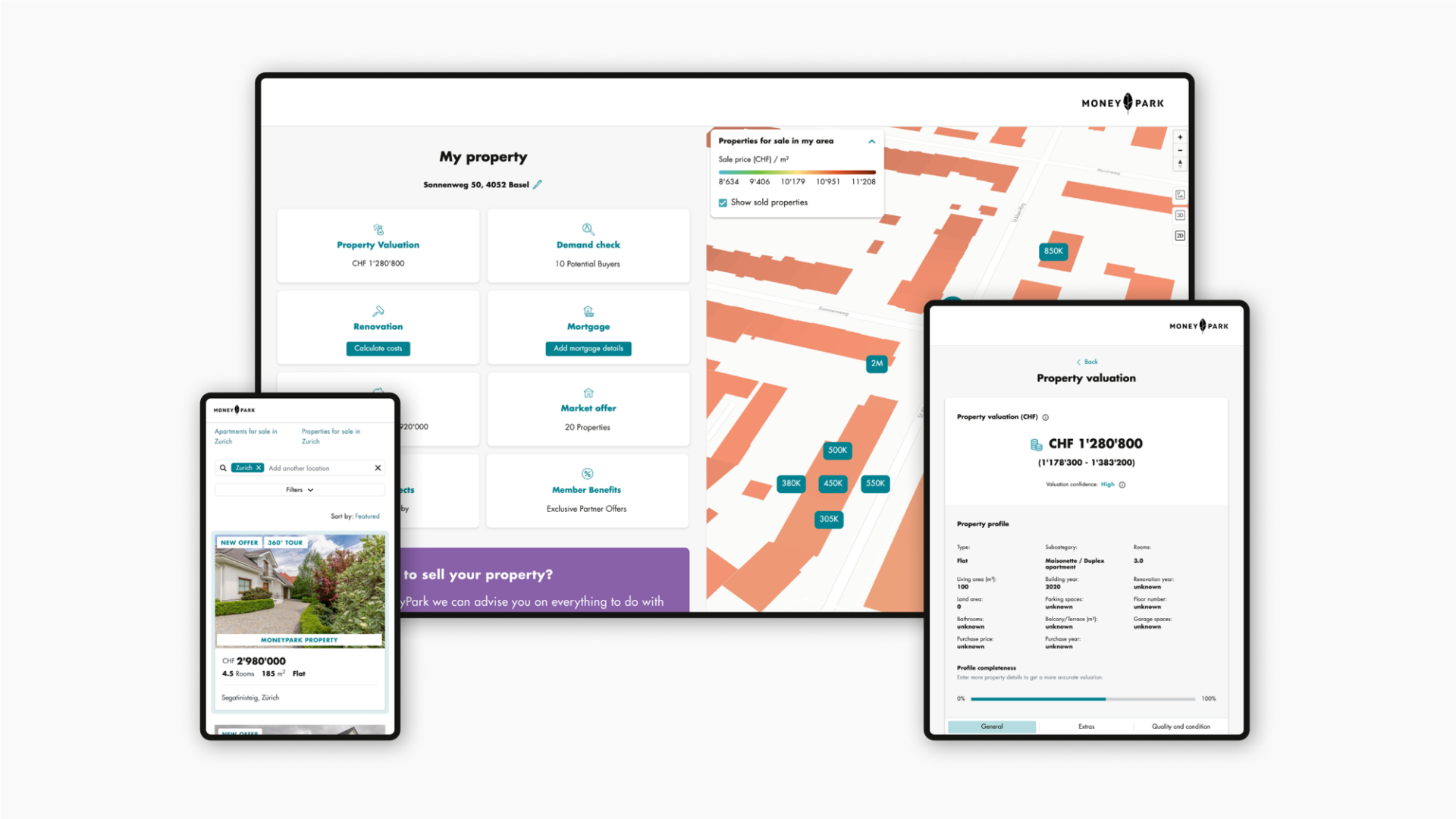

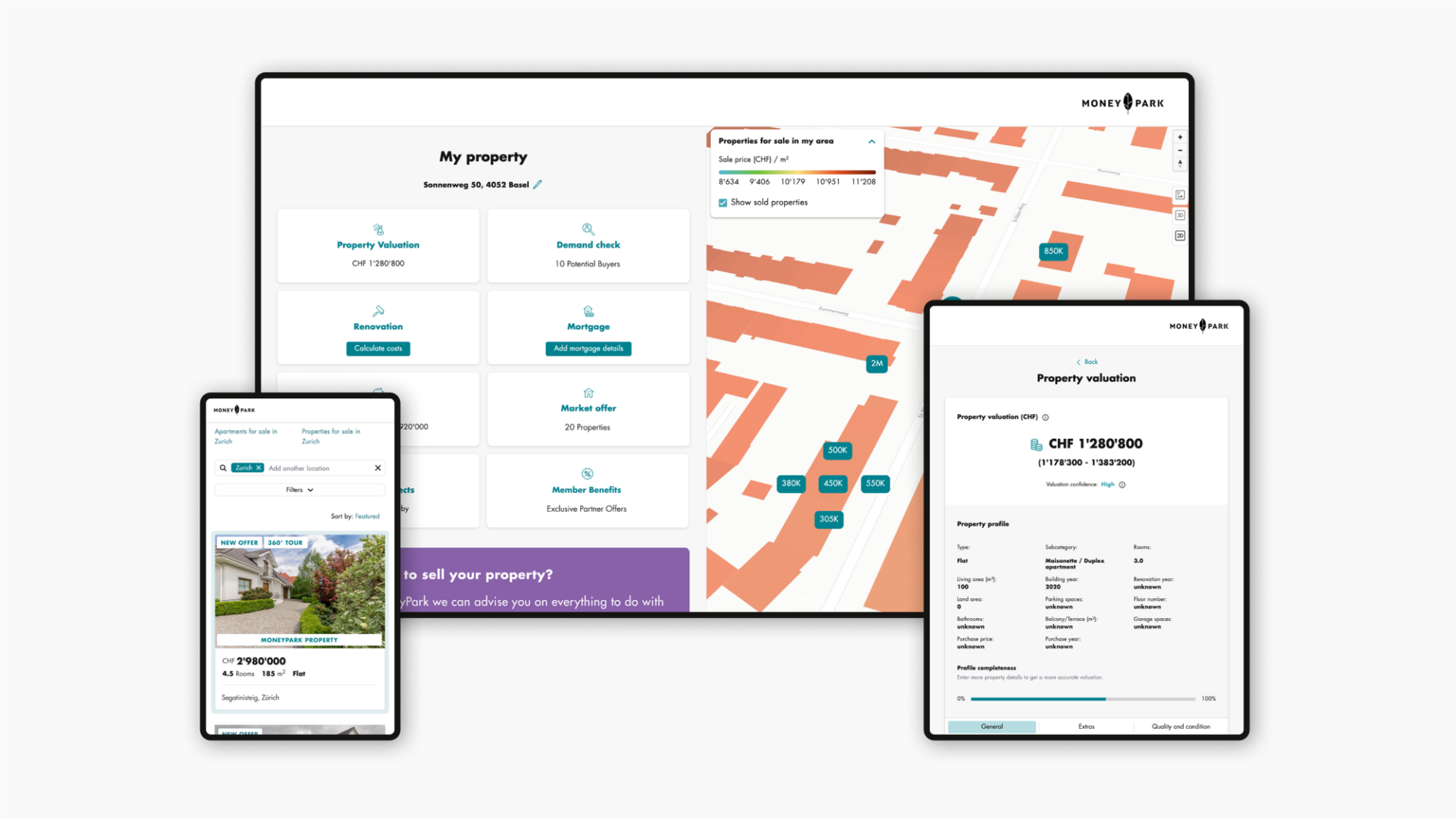

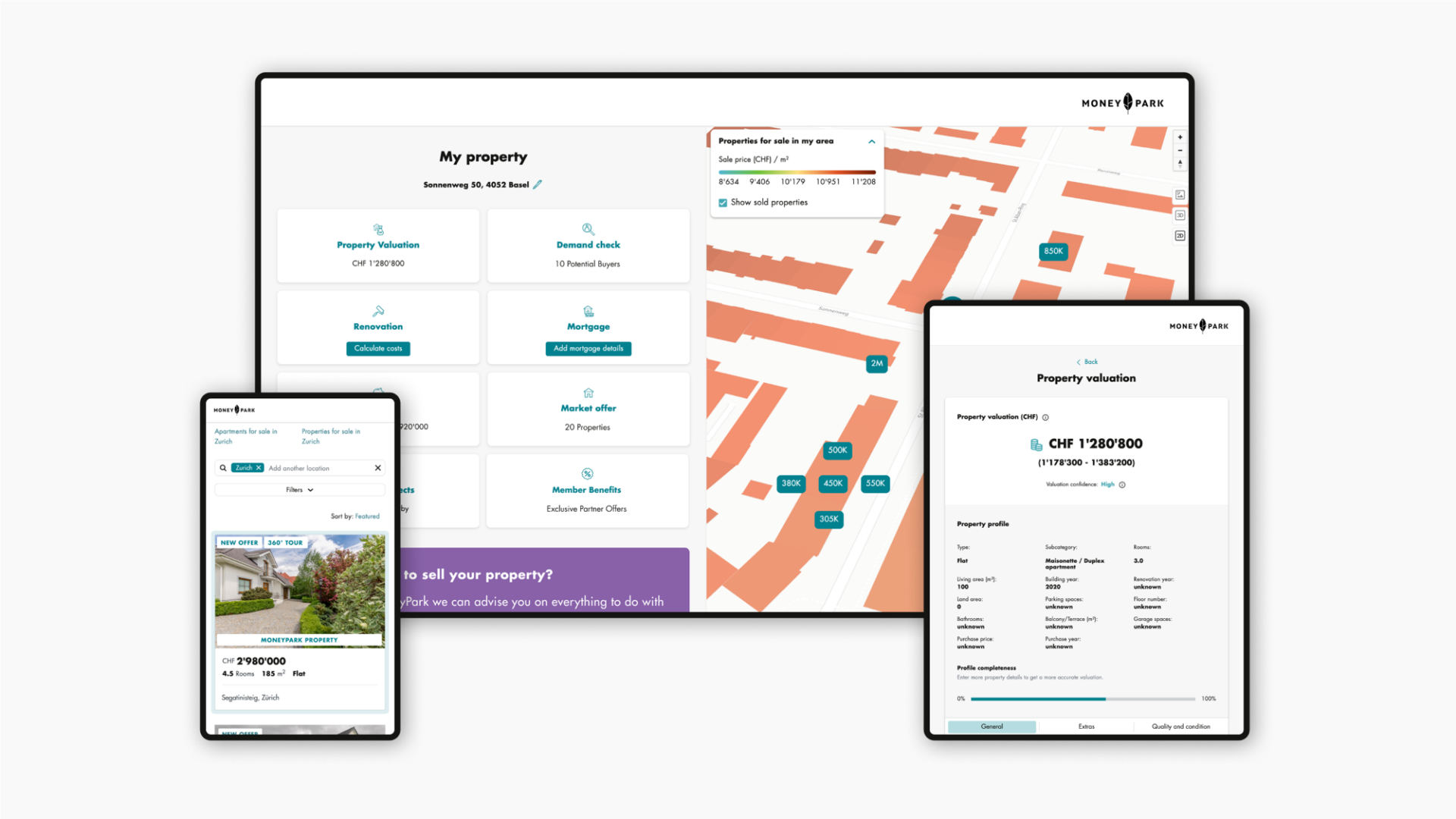

What should be considered with regard to the financing of a holiday property?

Stricter criteria apply for the approval of a mortgage for a holiday home than for your primary residence, and taxes are calculated in a higher bracket and there are different deductions that you can claim.

In order to be able to take out a mortgage for a holiday home (whether a house or apartment), the property must meet affordability criteria. As a general rule, the cost of your primary residence and that of the holiday property must not exceed one third of your gross income. While a minimum of 20% equity is required for your primary residence, depending on the lender you will need 30% to 50% equity when buying a holiday home. You should also be aware that, unlike for your primary residence, when investing in holiday property you may not use any of your 2nd or 3rd pillar assets.

What are the tax implications of a holiday property?

Whether it's your primary residence or a holiday property, you must always pay tax on the imputed rental value. When buying a holiday home (house or apartment), the property's local tax office will calculate a rent at market rates and convert it into an imputed rental value that is taxable as income. If you already own your own home, in future you will have two imputed rental values which, after deducting interest and maintenance costs, will each result in taxable income at the respective locations. However, in that case the tax bracket is not determined at the respective locations, but rather by the sum of both taxable incomes combined. This means that you will enter a higher tax bracket in both locations and pay taxes on the corresponding income at the respective location. Deductions are handled differently, too: while you can deduct pillar 3a contributions from tax at your primary residence, this can only be done indirectly for your holiday property by means of amortization via pillar 3b. This allows you to have higher deductible mortgage interest rates while your mortgage remains constant.

Please note: renting out your holiday property will also affect your taxes. The amounts you receive in rent are classified as income and must therefore be taxed.

Buying a holiday property abroad

What should I be aware of when buying a holiday property abroad?

As a Swiss citizen you are allowed to buy property abroad, but you should first clarify how residence permits are regulated at your desired location. Each country has its own tax law, and virtually all countries impose land, wealth and property taxes. In addition, the Swiss tax authority assesses the tax value of the foreign property as an asset and the imputed rental value as income, which you must additionally pay tax on. You should also account for notary and registration fees.

Test and compare!

Have your dream holiday home thoroughly inspected before you buy! This may sound obvious, but can be easily forgotten about amid all the excitement. Find out as much as you can about your desired location. Visit the place at different times of the year and talk to locals and neighbours. Ideally, you would first be able to rent your desired property in order to experience everyday life there. It would also be advisable to have the building structure, installations and systems checked by experts before making a purchase. Compare the purchase price of your desired property with similar houses or apartments in the area. Clarify whether the property is subject to any usufructuary rights, rights of way or passage, building restrictions, real property liens or mortgages. After the purchase, you should make sure that the changes are entered in the land register immediately.

It's worth seeking independent advice

Whether you opt for a holiday property in Switzerland or abroad, first get to know the region, location and infrastructure – and bear any future resale in mind. Obtain several financing offers and compare them with one another. It's always worth asking an independent specialist for advice.